Owning an ideal car is a big accomplishment for a lot of people in India. And everyone requires the Best Strategies for Financing Car with EMI but no Interest. But in order to make this dream into reality, one must have strong financial planning and strategic decision-making skills else it can damage you financially. It’s crucial to take an essential strategy that fits with your financial objectives and ambitions rather than rashly jumping into a car purchase that puts a burden on your finances. This way it will enable you to effectively mobilize your savings and needs.

I’ll go further into The Best Strategies for Financing your Dream Car (Interest free) while maintaining long-term financial stability in this extensive post. You will come to learn how to maximize the value of your assets and make well-informed choices by investigating different approaches and factors.

First, you must understand that buying a vehicle outright with all your funds like savings, investments, emergency funds, is the most financially responsible course of action. Paying the whole sum up front and avoiding monthly payments may sound tempting, BUT doing so will severely deplete your funds and make it more difficult for you to manage your future investment goals. So, it is not advisable at all by any expert advisors.

Instead, it is recommended to use financial options such as Equated Monthly Installments (EMIs) that allows you spread the cost of your car over a period of time, making it more budget friendly and financially appropriate.

But how to plan it:

When considering a vehicle purchase, your Debt to Income (DTI) Ratio is an important consideration. This ratio shows you how well you can handle debt in relation to your income. Your overall loan payments—including those for your car—should ideally not be more than 50% of your take-home salary. In order to protect your financial stability and make sure you can easily pay your debts, you must maintain a good debt-to-income ratio.

The DTI ratio totally depends on person to person and salary structure, liabilities, investment goals, responsibilities, family background and many other factors. So, I won’t consider these factors but give you an assumption on how to finance your car with a simple example which you can modify according to your goals, expenses and savings.

Buyer persona – a person aged 30 years, with his family (wife and a child), lives in Bangalore city and is earning Rs.1 lakh per month in-hand salary. The person wants to buy a car of Rs.10 lakhs and saved for this only Rs.2 lakhs, whereas he has mutual funds investment amounting to Rs.5 lakhs and emergency funds of Rs.3 lakhs and for child school admission – Rs.2 lakhs.

So, how will he manage the funds?

Note: Financial experts generally recommend that your total monthly debt payments, including the EMI, should not exceed 40-50% of your gross monthly income.

Assuming your monthly expenses, including rent, utilities, groceries, and other essentials, including shopping amount to Rs. 40,000 per month, and then, on child education, you spend Rs. 12,000 per month (as per metro cities), investing an amount of Rs.8,000 per month in mutual funds or stocks, investing Rs.10,000 per month in Recurring deposit account for emergency fund. After this, you’re left with Rs. 30,000 as disposable income after deducting expenses from your in-hand salary of Rs. 1 lakh per month.

Based on this scenario, you should aim to keep your EMI within 40-50% of your disposable income, which is around Rs. 15,000 per month.

Therefore, when considering a loan with an EMI, ensure that the EMI amount falls within this range to maintain a healthy balance between debt repayment and your overall financial well-being.

Buy a car of Rs.8-10 lakh with Rs.2 lakh savings:

Now, if you want a car of Rs.10 lakhs (on-road price), you give only a down payment of Rs.2 lakhs without touching other investment funds and emergency funds. I also consider you are well aware of investment in mutual funds and gold, as you are making a SIP as per my above scenario.

You will have to get loan of remaining amount of Rs. 8 lakhs Car loan of Rs.8 lakhs with 12% p.a (varies person to person and bank to bank), and for period 5 years, will cost monthly EMI of Rs.17,796/-,and the total interest will amount to Rs.2,67,733/-.

Don’t worry, however, about the interest portion. Over the years or months, you have dutifully saved money in your emergency fund and mutual fund. This is the first benefit which saves you from restarting your investment for emergency funds and mutual funds. Rebuilding and growing them again will take the same amount of time and won’t be available for disposal in urgency.

However, if I assume you are not doing any SIP in mutual funds or gold, you will have more disposable income. When you get a loan with EMI of Rs.17,796/- of Rs.8 lakhs, immediately start researching good investment plans or mutual funds where you can save some amount for 5 years.

Nullify your interest part on your car loan:

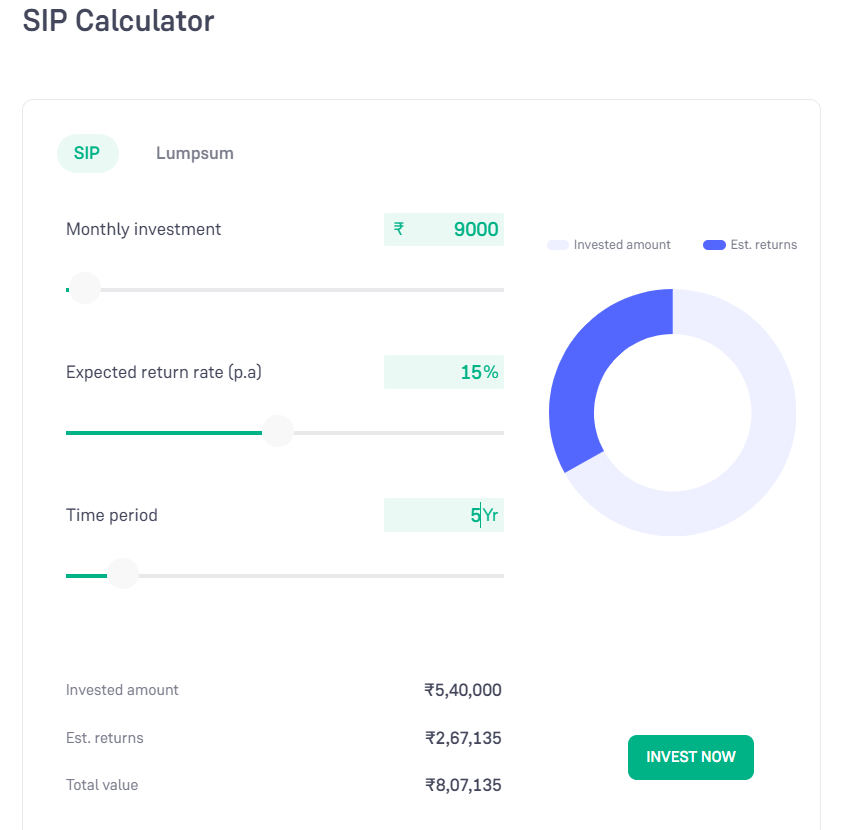

Let’s suppose, you make a SIP of Rs.9,000 per month (half of EMI value) for 5 years in a mutual fund where you can get 15% average return. So, your return will be Rs.2,67,135/-. Now, you can compare the interest part on the loan and the return received on your investment in these five years. It’s like you have recovered all your interest paid without disturbing your other investments and funds.

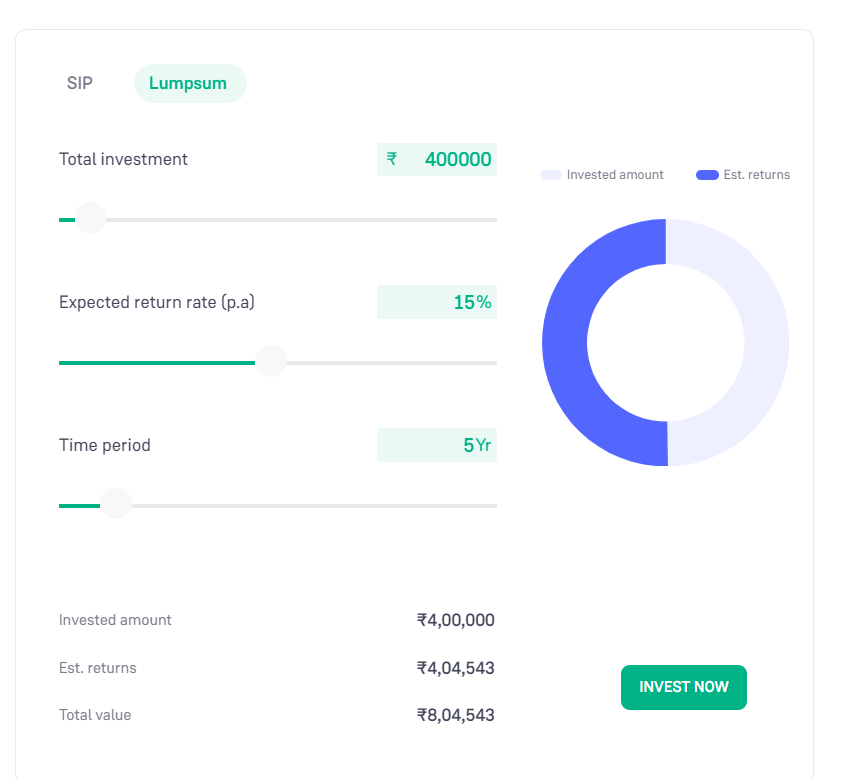

Second assumption, You have a lump sum amount of Rs.4 lakhs. You invest this amount in a mutual fund which can offer 15% returns and the lock in-period should be 5 years. Your returns will be Rs.4,04,543/-. Now, again you can compare the interest and the return received.

Now, you know why I am telling you to buy a car on a down payment of Rs.1-2 lakhs and the remaining amount to invest in good investment plans.

Conclusion:

Every scenario is an assumption, it may vary person to person, its investment strategies, financial planning, future goals, etc. Interest on investment is also assumed. So research carefully before investing.

Choosing an auto loan allows you to take advantage of favorable interest rates and adaptable payback schedules, sparing your money for other important expenses. Furthermore, you may lessen the burden of loan interest payments and keep accumulating wealth over time by following a disciplined savings and investing plan.

In summary, achieving your dream of owning a car requires a balanced approach and essential financial strategies that prioritizes financial responsibility and long-term goals of prosperity. By adopting strategies such as prudent financing, maintaining a healthy DTI ratio, and leveraging savings and investments wisely, you can realize your future goals while safeguarding your financial future.

Remember, the key to successful car ownership lies not just in the acquisition of the vehicle itself, but in the broader context of prudent financial management and strategic decision-making. With careful planning and informed choices, you can walk comfortably on the journey towards having a dream car with confidence and peace of mind.