The Goods and Services Tax (GST) regime in India has brought significant changes to various sectors, including the travel and tourism industry. If you are willing to build a career as a Tour and travel agent, you need to understand the implications of GST and how to rightly pay the taxes. This article clarifies the GST rates, HSN codes, and key rules applicable to tour and travel agents in India.

Read more: Full Guide & Process for Home-Based Travel Agency in India

It is a booming industry that is growing at a rate of 7.77% and expected to reach USD 131.7 Billion by 2030 (Source: Blueweave). Before, we start, you should know the difference between tour and travel agents and what actually they do: –

Tour Operators:

They create and sell complete travel packages for vacations or other purposes. These packages typically bundled services like accommodation, transportation, sightseeing tours, and activities into a single itinerary.

Travel agents:

They act like intermediaries in facilitating travel of their clients. Their main service is connecting travelers with individual travel service providers like hotels, airlines, bus booking and car rentals. They also book cruises, events, and other travel components, and help travelers in ticket booking or sightseeing, and other recreational activities.

But, they don’t control the pricing or service delivery of individual components. They only earn a commission on bookings made.

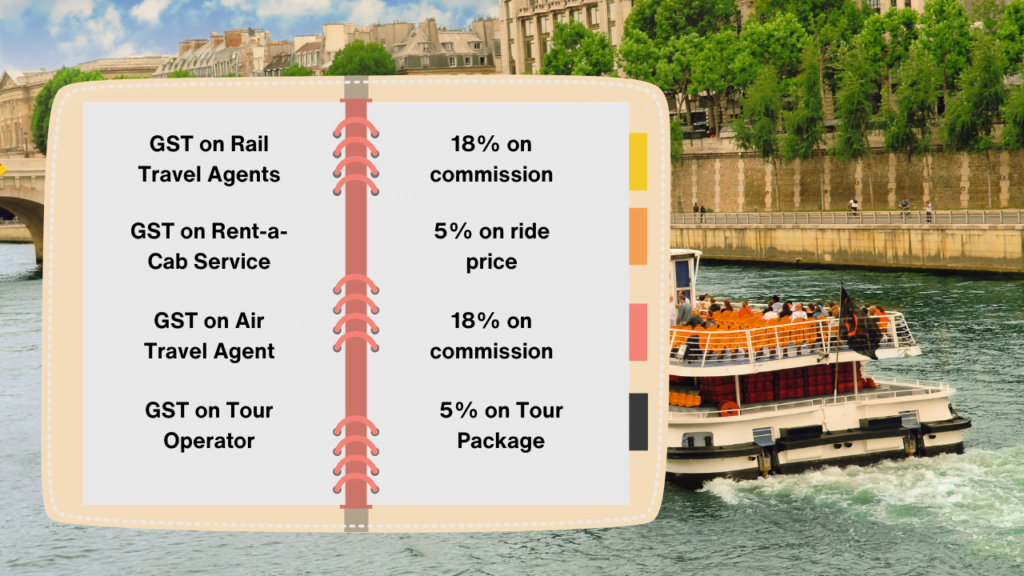

GST on Tour Operators:

GST @ 5% has been applied on services of tour operators without benefit of Input Tax Credit (ITC) on goods and services. 5% GST will be payable on the gross amount charged by the tour operator from the customer. This GST is uniform for all services – package tours, hotel accommodation only etc.

Tour operators that pay 5% GST are not eligible to claim input tax credits for CGST, SGST, and IGST that they pay to hotels, transporters, airlines, restaurants, travel agencies, guides, houseboats, cruise ships, luxury trains, monument admission fees, joy rides, etc. Secondly, the tour operator would not be allowed to claim the GST levied by the counterpart tour operator as an input tax credit.

In the case of camping, the service providers providing services such as tent, shamiana, catering etc. will get classified under the respective heads and not as tour operators. In case a tour operator purchases goods and services from unregistered vendors, GST needs to be paid by the tour operator on reverse charge principle.

HSN: 998552 at the rate of 5% without ITC

GST on Air Travel booking Agents:

If you are working as an agent who books tickets on behalf of your clients, you must be charging commission from the client over the above ticket fare. On this commission, you will have to pay 18% tax on commission collected as it is a service provided by you.

But, Rule 32(3) of the CGST Rules 2017, gives another method to pay GST on air travel ticket booking. The details are as follows:

- Domestic Air Travel Ticket: 18% GST on 5% of base fare. For example, Suppose, base fare is Rs. 1,00,000. 5% will be Rs. 5,000 and on that, 18% GST which is Rs. 900.

- International Air ticket: 18% GST on 10% of base fare. For example, Suppose, base fare is Rs. 1,00,000. 10% will be Rs. 5,000 and on that, 18% GST which is Rs. 1800

The above rates of GST are applicable to IATA agents having inventory to issue air tickets on behalf of the airline. In case an air travel agent buys ticket from IATA agent and charge service

charges only from the customer / passenger as his mark-up, such an agent is not authorized to work on basic fare modules. He will pay 18% GST on his service charges disclosed separately in the invoice issued by him to the customer HSN:

HSN: 998551 at the rate of 18% with ITC

GST on Rail Travel Agents:

As a Rail Travel Agent, you are required to pay 18% GST on service charges collected from the customers / passengers. No other optional rate is applicable in their case.

HSN: 996731 or 996739 at the rate of 18% with ITC

GST on Rent-a-Cab Service:

A cab operator collects 5% GST from their customers and pays them to the Government. There is a condition no input tax credit (ITC) can be availed. Further, if the cab operator is not registered, the tour operator, or travel agent, or app aggregator like Uber, Ola pay 5% GST by collecting from their customers.

HSN: 996601 at the rate of 5% without ITC

GST on Other services

Usually on vacation packages, other sightseeings, museum, recreational activities and other entertainment tickets are also provided to the customers by tour operators. So, 28% GST on Services by way of admission to entertainment events or access to amusement facilities including exhibition of cinematograph films, theme parks, water parks, joy rides, merry-go rounds, go-karting, casinos, race-course, ballet, any sporting event such as Indian Premier League, is applicable.

But, the condition is that no ITC is available for tour operators. They have to pay 5% GST after collecting from their customers.

HSN: 9996 at the rate of 5% without ITC by tour operator

What if you are both travel agent and Tour Operator

You need to maintain separate billing and charge GST based on HSN and services provided by you to your customers. This will help you in paying tax correctly to the Government.

Exempted Services by tour operators

Services of a tour operator are specifically exempted:-

- Services by a specified organization in respect of a religious pilgrimage facilitated by the Ministry of External Affairs of the Govt. of India, under bilateral arrangement.

- Services provided by a tour operator to a foreign tourist in relation to a tour conducted wholly outside India.

Summarized the GST rates

| Services | HSN (Services) | GST Rate |

| Services provided by a tour operator to a foreign tourist in relation to a tour conducted wholly outside India | 9985 | NIL |

| Tour Package or vacation package | 998552 | 5% without ITC |

| Air Travel booking Agent | 998551 | 18% |

| Service Charge Paid on Travel-Related Like Visa, Passport, etc | 998559 | 18% |

| Tourist guide services | 998556 | 18% |

| Reservation services for event tickets, cinema halls, entertainment and recreational services and other reservation services | 998554 | 5% GST on service charge without iTC and 28% GST on tickets price |

| Commission of Rail Travel Agents | 996731 or 996739 | 18% GST on service charges |

| Rent-a-Cab Service | 996601 | 5% without ITC |

Conclusion

You as a Tour operator and running travel agency, may successfully navigate the GST system by being aware of the relevant GST rates, HSN codes, and important guidelines. This information optimizes your tax liability, reduces the possibility of fines, and guarantees GST compliance. You can take advice from the expert and avoid any issues in your business.