Financial planning is about making informed decisions that maximize your financial health and minimize unnecessary expenses. Recently, I faced a dilemma when buying a scooty worth ₹1,14,000.

Even though I had enough savings to pay the full amount upfront, I opted for an EMI plan. This decision wasn’t just about convenience but also about strategic financial planning. Here’s a detailed look at why I chose this route and how you can make smart financial choices too.

The Initial Decision

When I decided to buy a scooty, the total cost was ₹1,14,000. I had the option to pay this amount upfront, but I chose to make a down payment of ₹25,000 and finance the remaining ₹89,000 through EMIs. Here’s why this approach made more financial sense:

Benefits of Not Paying in Full

- Liquidity Preservation: Paying the full amount would have significantly reduced my liquid savings, which could be better used for emergencies or other investments.

- Opportunity Cost: By not using all my savings on a single purchase, I could invest the remaining amount in higher-return opportunities.

Exploring Financing Options

Showroom Dealer Financing

The showroom dealer offered financing at a 10.5% interest rate, resulting in an EMI of ₹6,500 per month for 18 months. This totaled ₹1,17,000 (₹6,500 x 18 months). While this seemed manageable, it included substantial interest.

Credit Card EMI Conversion

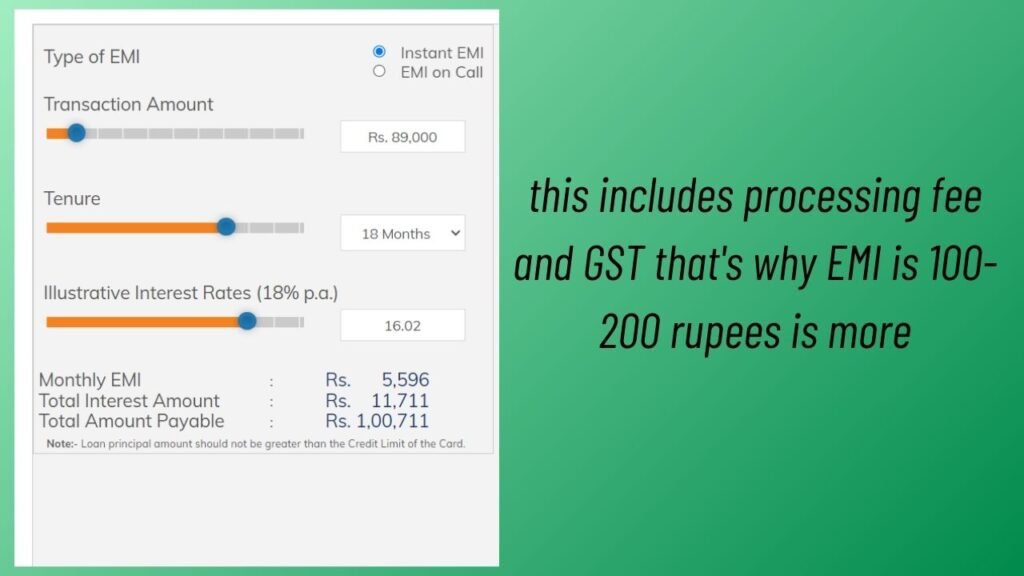

I also considered converting the purchase into a credit card EMI, which had an interest rate of 15.99% per annum. Surprisingly, this option offered a lower EMI of ₹5,700 per month for the same period, totaling ₹1,02,600. This was significantly lower than the dealer’s financing option, saving me ₹14,400 in interest.

Calculation and Comparison

- Showroom Financing at 10.5%: ₹6,500 x 18 months = ₹1,17,000

- Credit Card EMI at 15.99%: ₹5,700 x 18 months = ₹1,02,600 (this includes processing fee and GST that’s why EMI is 100-200 rupees is more)

- Savings: ₹1,17,000 – ₹1,02,600 = ₹14,400

Documentation and Ease

Another critical factor was the documentation required. The showroom’s financing needed extensive paperwork, including income proofs and other documents, which was cumbersome. In contrast, the credit card EMI conversion required no additional documentation, making it a more straightforward and quicker process.

Why Choose EMI When You Can Pay in Full?

- Cash Flow Management: Opting for EMIs allows for better cash flow management. You can use the remaining funds for other essential expenses or investments.

- Emergency Fund Maintenance: Keeping an emergency fund intact is crucial. Paying in full can deplete this fund, leaving you vulnerable to unexpected expenses.

- Investment Opportunities: The money saved can be invested in various instruments like mutual funds, stocks, or fixed deposits, potentially earning higher returns than the interest paid on EMIs.

Practical Financial Tips

Budgeting

Create a detailed budget to track your income and expenses. This helps in identifying areas where you can cut costs and save more.

Building an Emergency Fund

Ensure you have an emergency fund that covers 3-6 months of living expenses. This fund acts as a financial safety net in case of unforeseen events like job loss or medical emergencies.

Investing Wisely

Invest your savings in diversified portfolios to spread risk and maximize returns. Consider stocks, bonds, mutual funds, and real estate as potential investment options.

Managing Debt

If you have multiple debts, prioritize paying off high-interest ones first. Consider consolidating debts into a single loan with a lower interest rate to manage repayments effectively.

Conclusion

Choosing the right financial strategy is essential for long-term financial health. While it might seem counterintuitive, opting for an EMI plan instead of paying in full can be a smarter financial move. It helps maintain liquidity, preserves your emergency fund, and allows for potential investment opportunities.

By understanding your financial goals, budgeting effectively, saving for the future, and managing debt wisely, you can make informed decisions that benefit you in the long run. Remember, financial planning is not just about managing money; it’s about making your money work for you.