You must have heard people suggesting you start SIP (Systematic Investment Plan) as early as possible to build wealth before retirement. SIPs not only create wealth but also help you develop a habit of investing and saving for future goals.

Many of us have big dreams like buying a dream car, owning a house, paying for a child’s marriage, or funding a child’s higher education. Based on these goals, we start monthly investments in mutual funds, which often give better returns than traditional savings or investment options.

I also started investing and, out of curiosity, check my returns daily to see how much I have gained. You probably do the same. But my investment strategy is a bit different, and today, I want to share it with you. Based on a few parameters, you can decide which investment style suits you best.

How I Plan

Instead of investing in mutual funds monthly (like a typical SIP), I prefer to invest annually in a lump sum amount. It’s similar to a systematic investment plan, but I do it once a year.

For example, I invest Rs. 2,50,000 yearly in mutual funds from my total savings. I choose three mutual funds: an equity-linked mutual fund, a multi-asset fund, and a flexi-cap fund. Here’s why I do this.

Fixed SIP or Step-Up SIP: Which Investment is Best for You?

Why I Do This

One key reason is to save on tax with Long-Term Capital Gains (LTCG). There’s a tax exemption on the first lakh of profit earned as LTCG, and for the remaining profit, I only need to pay a 10% tax.

Another reason is that I know the Net Asset Value (NAV) at which I invested, making it easier to calculate the actual returns on my initial investment over a year.

How I Benefit

Let me share how I figured out this investment approach. I did some calculations, which I’ll share with you.

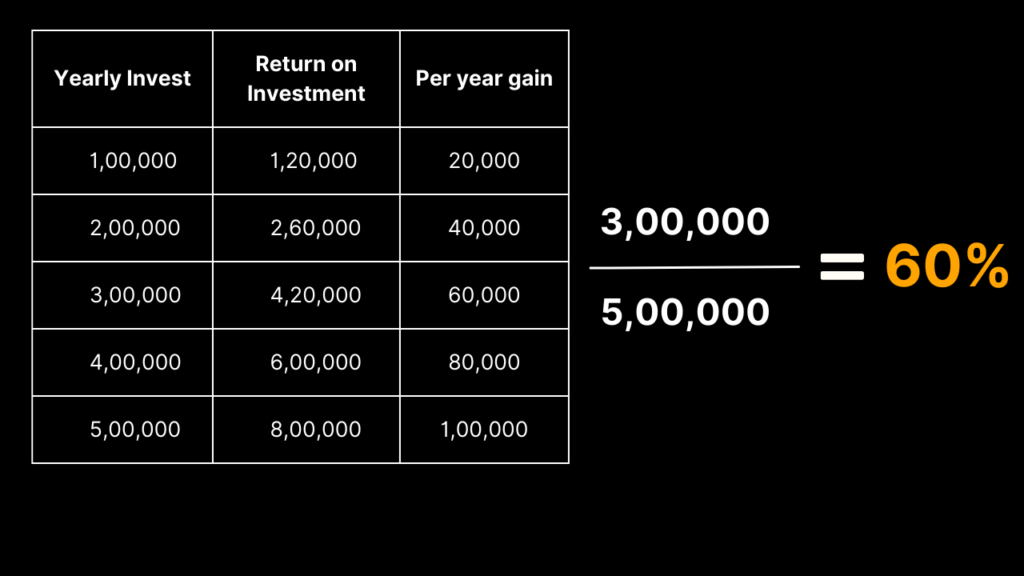

Scenario 1: Annual Investment

Suppose you invest Rs. 1 lakh per year and get a 20% return. In this scenario, you invest Rs. 1 lakh each year for 5 years without withdrawing the interest earned. Here’s what it looks like:

- You get a total return of 60% over 5 years, assuming no withdrawals and fixed NAV.

- You withdraw the full amount after the 5th year.

- The LTCG tax is calculated on Rs. 2 lakhs after a one-lakh exemption, resulting in a tax of Rs. 20,000.

Scenario 2: Annual Investment with Reinvestment

In this scenario, you invest Rs. 1 lakh every year at a 20% return, withdraw the profit, and reinvest it along with your Rs. 1 lakh annual investment. Here’s the result:

- The total return is 79% on a total investment of Rs. 5 lakhs.

- Reinvesting the profit increases your returns.

- The LTCG tax is calculated on the profit above Rs. 1 lakh, resulting in a tax of Rs. 5,619 in the 4th and 5th years (10% on LTCG profit).

Conclusion

I’m not saying you should follow my exact strategy. Everyone has their own investment style and benefits from it. Returns are not guaranteed and depend on factors like NAV price, withdrawal and investment dates.

It’s generally preferred to invest monthly to build a consistent investment and savings habit. Keeping money in a savings account for 12 months yields minimal returns, and we lose potential returns during this period. This factor also needs to be considered before making investment decisions.

Consulting a certified financial planner can help you create a better investment strategy tailored to your needs.